We need to STOP underestimating compound interest

Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.

We as humans are very easy to fool. We are fooled by other people all the time and we fool ourselves daily.

One of the most commons ways we fool ourselves is to underestimate compound interest. Most people know the word, and they remember vaguely how it works from high school, but even in high school they never quite hit home how powerful it can be.

So powerful, that Albert Einstein said the following:

Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it. - Albert Einstein

And that's coming from the man best known for developing the theory of relativity which led to the development of the Atom Bomb which ended World War 2 and change trajectory of humanity forever.

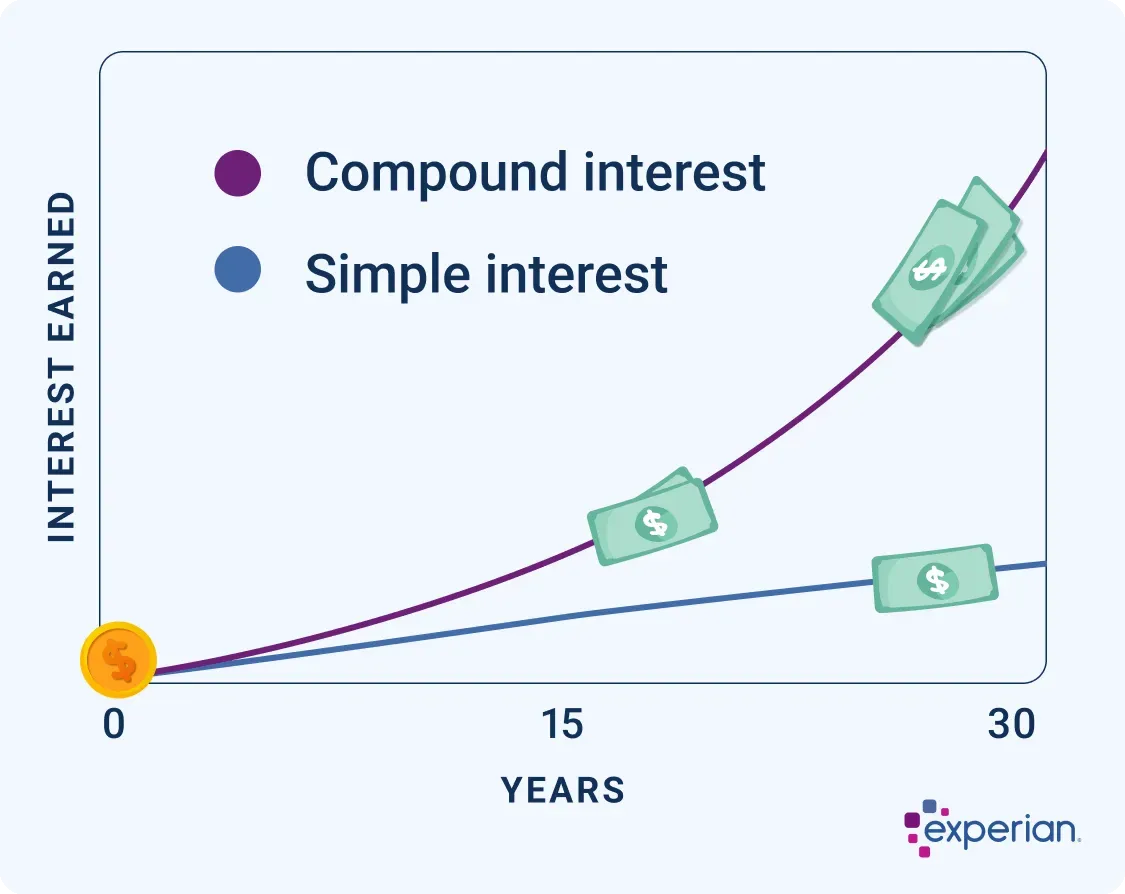

Compound Interest Definition

Before we go further, I would just like to do a quick refresher on what compound interest is and how it works.

\[A = P(1+r)^{n}\]

Where:

- A = amount after time

- P = principal (starting money)

- r = interest rate per period

- n = number of periods

Right about here is where we would start doing some calculations in high school about what happens if we invest R1000 at 10% per annum for 20 years. Those examples are fine, but I think it's better if we use some examples that show how easily we underestimate the power of this little formula.

Choices

Here's a question for you, what would you choose:

- R1 000 000 today or 1c that doubles every day for 30 days?

If you didn't know this question was rigged, you'd probably take the R1 000 000 every day. I mean imagine what you could do with all that money.

Let's see what happens if we take the latter option, which requires some patience, but the upside is worth it.

Start with R0.01 on Day 1 and double the amount each day. The amount on Day \(n\) is:

\[A = 0.01(2)^{n-1}\]

Therefore the amount on Day 30 would be:

\[A = 0.01(2)^{30-1} = R5,368,709.12\]

😮 That's right if you just waited 30 days, you would have more than 5 times the amount than taking the R1 000 000 on day 1.

Multiplication is not our friend

If you ask most people what the answer is to:

\[8+8+8+8\]

They won't have difficulty in getting to the answer. But now ask them what is:

\[ 8 \times 8 \times 8 \times 8 \]

Much harder right? Our brains are not wired to do multiplication - which might be part of the reason we struggle to comprehend compound interest.

I got the example above from an amazing episode of the Diary of a CEO episode with Morgan Housel (author of Psychology of Money) as a guest. If you want to listen to the full episode, you can find it below.

The Savings Expert: The Truth About America Collapsing! The Cost Of Living Is About To Skyrocket! - Diary of a CEO

A Coffee a Day

Another example mentioned in the podcast; drink a coffee a day, which costs R30.00 vs investing that R30.00 in the stock market every day at 8% return per annum for 40 years.

For this the formula looks a bit more complicated, but bear with me:

\[A = \frac{P(1+r_d)^{n}}{r_d}\]

Where:

- A = amount after time

- P = daily investment

- \(r_d\) = daily interest rate i.e. annual divided by 365

- n = number of periods

So let's see what the result is:

\[A = \frac{P(1+\frac{0.08}{365})^{365 \times 40}}{\frac{0.08}{365}} = R1,360,800\]

So, if you don't drink a cup of coffee per day, and rather invest it each day, after 40 years, you will be a millionaire.

Just a quick caveat though, with all of these examples, we are ignoring inflation and not accounting for the fact that R1 000 000 in 40 years won't be worth the same that it is today, although the principle stays valid.

But surely I need to live as well?

This post is using extremes to illustrate how we underestimate compound interest, but we also need to live life and be happy.

So I'm not saying stop spending any money - but the point I want to drive home, is that before we do, it's probably a good idea to look at the bigger picture and consider the opportunity cost of spending that R30 each day on a cup of coffee.

The Tail-end of Compound Interest

Something else I would like to focus on is the tail-end of compound interest and how most of the gains are only realised as you get closer to the end.

Earlier I mention Morgan Housel and his book The Psychology of Money. In the book he writes about Warren Buffet, one of the most successful investors of all time.

He wrote “His (Warren Buffet) skill is investing, but his secret is time.” That’s the magic of compounding. Housel points out that 99% of Warren Buffett’s wealth came after he turned 65. Buffett’s net worth is around $132 billion. Most of that fortune came later in life—$84.2 billion after 50.

Compounding works like a snowball rolling down a hill: the longer it rolls, the bigger it gets. As Buffett puts it, “The trick is to have a very long hill—start young or live a long life.” Time isn’t just money—it’s the secret weapon of wealth.

Let's look at the example of a 1c doubling every day again. After 30 days, you have R5.3 million. What if you waited 1 more day? Then you would have R10.6 million.

Don't retire early

Let's do a quick comparison of retiring at 55 vs retiring at 60.

Let's assume you've saved your whole life, and you now have R5 million saved. You are currently getting 8% return per annum. To keeps things simple, we assume you don't add more money to your retirement fund, you just wait for it to grow 5 extra years.

\[A = 5000000(1+0.08)^{5} = R7,346,640.5\]

That's right, if you work 5 years longer, you will have 47% more money saved versus retiring at 55.

Patience is key

The scarlet thread throughout most of these examples is patience. You will never reap the benefits if you cannot be patient and wait for compound interest to take effect.

The next time you catch yourself falling into the trap of thinking "it's only R30", maybe you need to reconsider that coffee. Or you need to make sure that you are sharing it with someone and that relationship is more meaningful to you than all that money in 40 years time.